Preview

Publication Date

Spring 4-20-2020

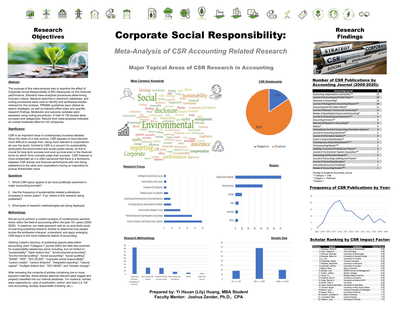

Abstract

The purpose of this meta-analysis was to examine the effect of Corporate Social Responsibility (CSR) disclosures on firm financial performance. Standard meta-analytical procedures determining inclusion criteria, literature searches in electronic databases, and coding procedures were used to identify and synthesize articles retained for this analysis. PRISMA guidelines were utilized as search strategies, as well as interpret effect sizes and quantify research findings. Moderator and outcome variables were assessed using coding procedures. A total of 136 studies were surveyed and categorized. The results from meta-analyses indicated an overall moderate effect for US companies. Several outcomes indicated moderate-to-large effects; specifically, moderate to large positive effects were revealed for European and Asian companies. Moderator analyses were conducted to explain the variance between groups. While no significant differences were found between other moderators, several trends were apparent between studies.